How to Qualify Crypto Home Buyers: A Realtor's Guide

When a buyer calls and asks if you take crypto, your first instinct is probably to panic. Don't. You already know how to handle this — you do it every single day with traditional buyers.

When a buyer calls and asks if you take crypto, your first instinct is probably to panic. Don't. You already know how to handle this — you do it every single day with traditional buyers.

Think about your typical buyer process. A buyer calls, interested in a property, and your first move is always the same: get them preapproved. You hand them off to a loan officer, they get their preapproval letter, and now you know they're serious.

A crypto home buyer is the same — you just need a crypto real estate professional vetting the buyer instead of a loan officer.

Our prequal process takes 15 minutes. Your buyer gets a proof-of-funds letter that looks exactly like what a mortgage lender would issue. You get confirmation they're real, their money is real, and they're ready to move. That's it. Same playbook, different asset class.

If you've been in the business a while, you probably curb-qualify buyers a little before you ever send them to your lender — a few quick questions to make sure they're worth your time. You can do the same with crypto buyers. Here's how.

Start with the fundamentals — there are fewer of them than you'd think — then we'll get into the specific red flags and green lights further down.

You don't need to understand everything about crypto to work with a crypto home buyer. You just need to understand a few concepts.

Just like we have the dollar, the euro, and the British pound, Bitcoin, Ethereum, and USDT are just different currencies. They act differently from a value perspective, but at the end of the day, they just represent US dollars. These currencies can be converted to U.S. dollars before or at closing — and those dollars can be used towards down payment, closing costs, traditional loan qualification, or to make an all-cash purchase.

If the buyer holds a type of crypto that you've heard of (Bitcoin, Ethereum, USDC, etc.), then they can likely use their crypto towards a home purchase. If they tell you they started their own token, it's likely that they are wasting your time. Here is a cheat sheet — if your potential buyer holds one of these, it's worth your time to pursue:

Outside of this list, there's a low probability the buyer holds anything useful for a real estate purchase. There are literally thousands of tokens out there, and most are useless for buying a home. See our full list of accepted currencies →

If a buyer sends you a screenshot of their Coinbase account or a blockchain explorer showing a huge balance, congrats — it proves nothing. Anyone can fake that. A screenshot doesn't prove they own the wallet, it doesn't prove they control the private keys, and it doesn't prove the funds are actually available. That's the equivalent of a buyer saying they're prequalified for $10M but having no documentation to back it up.

What you're actually looking at. A blockchain explorer is a public website that lets anyone look up activity on a blockchain. It shows real balances and transactions — but for any address, not proof that your buyer controls that address. A coin tracker or portfolio app just displays whatever balances a user enters or links; it reflects what someone says they hold, not what they actually have. And a screenshot of either is trivial to fake — with basic tools, anyone can mock up a wallet or exchange screen, logos and balances and all, that looks completely legit. That's why a screenshot is never proof of funds.

That's why we verify on the blockchain, confirm their identity, and issue a formal proof-of-funds letter. That's what escrow and underwriters actually care about.

Ask the buyer where their crypto is held, and listen for specifics. Are they on Coinbase? Kraken? Gemini? Or do they hold it in a self-custody wallet?

Exchange-held means their crypto sits on a platform like Coinbase, Kraken, or Gemini — similar to money in a brokerage account. Self-custody means they hold it themselves in a personal wallet (a Ledger, a Trezor, or a software wallet), controlling the private keys directly.

Both are legitimate. But here's the thing: a real crypto holder knows the answer immediately. They know their exchange or their wallet. They might be private about details — and that's fine, that's actually a good sign. Legitimate holders are cautious about sharing information.

What's a red flag is when they can't answer the question, they're vague, or they act like they don't understand why you're asking. That's evasion, not privacy.

Here's where you protect yourself, your time, and your clients.

Don't waste your time showing homes to a crypto buyer who hasn't been fully vetted. Scammers are slick, and plenty of would-be buyers have themselves been scammed — and Realtors are often the ones who foot the bill, not in dollars but in wasted showings, drafted offers, and weeks spent chasing a deal that was never real.

If a buyer says any of these, they're likely not legit — either scamming, or being scammed:

"I have crypto coming in." Nine times out of ten, they've been promised a deposit by a scammer, or they're waiting on a scheme that doesn't exist.

"Once my tranche unlocks…" Legitimate crypto holdings don't have tranches. This language usually signals they don't actually control the funds.

"It's locked up" / "I'm waiting on my exchange." They don't have access right now — which means they don't actually control the assets.

"My advisor is managing it" / "I'll check with my trader." They've likely been conned.

If someone with a million dollars in crypto says "I don't really understand how this works" or "I need help moving my crypto," be skeptical. Anyone who accumulated real wealth in crypto knows that asset — their wallet, their exchange, the basics. "I'm new at this" usually means they saw a big number in a tracker app and think they own something they never actually bought, or they got scammed and don't realize it.

If a buyer claims a hundred million dollars in crypto but doesn't know what to do with it, that's a lie. People with that kind of money have people — accountants, wealth managers, lawyers. Anyone who claims enormous holdings while acting lost is either lying about the amount or doesn't control it.

Keep this nearby — if a buyer says any of these, slow down and verify:

Not every signal is a warning. Here's what tells you a crypto buyer is the real thing.

Here's what separates a real buyer from a fake: a legitimate crypto holder will ask questions. They'll be cautious about verification. They might even be skeptical about sharing information.

That's good. That means they understand their money is valuable and they're protective of it. A scammer or someone with fake holdings won't care — they've got nothing to lose.

A real holder can tell you, without hesitation, what they hold and where it lives — the coin, the exchange or wallet, roughly how long they've had it. They may be private about the specifics, and that's fine. But fluency with their own money is one of the strongest signals you're dealing with the real thing.

A legitimate buyer treats getting verified the same way a serious traditional buyer treats getting preapproved: a normal, expected step. If they're ready to complete verification without stalling, hedging, or inventing excuses, that's a green light.

When you're on the phone with a crypto buyer, here's your script.

"Congratulations on the offer. Before we move forward, I need to confirm your funds are actually available. Can you get verified with our crypto team? It takes 15 minutes, and you'll walk away with a proof-of-funds letter that looks exactly like a mortgage preapproval. Sound good?"

If they say yes, send them to us.

If they hesitate, ask: "What's the concern?" Usually it's either they don't actually have the funds, or they're not sure how this works. Either way, you've filtered them out early.

If they're resistant or evasive, trust your gut. Move on.

That's it. You're not qualifying them yourself. You're just asking if they're willing to verify. We do the heavy lifting.

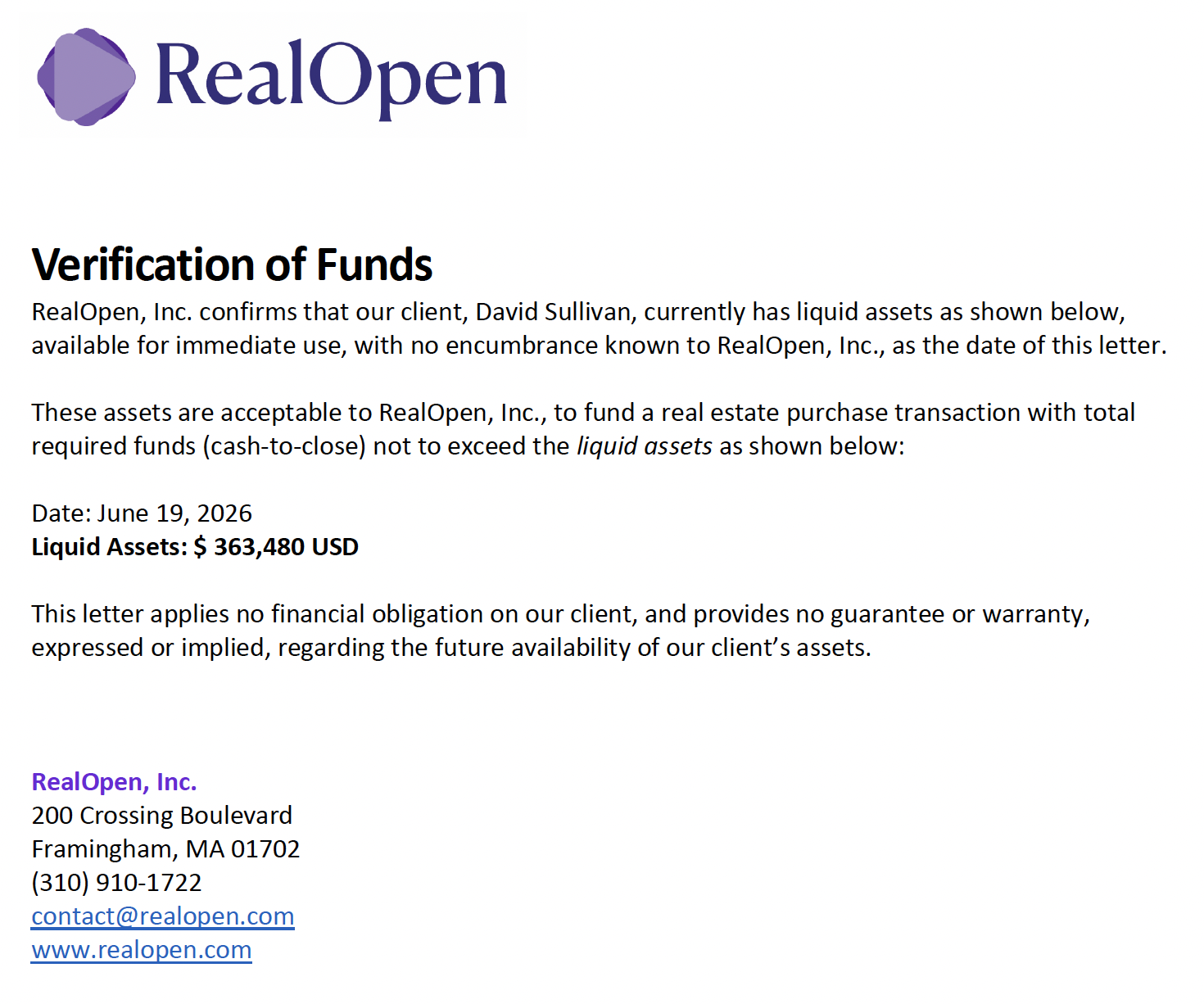

Here's what a real proof-of-funds letter looks like when it's done right.

This is what underwriters, title companies, and sellers actually need to see. It's got verified identity, verified wallet holdings, and a clear statement of available buying power. No guessing. No screenshots. Just facts on paper.

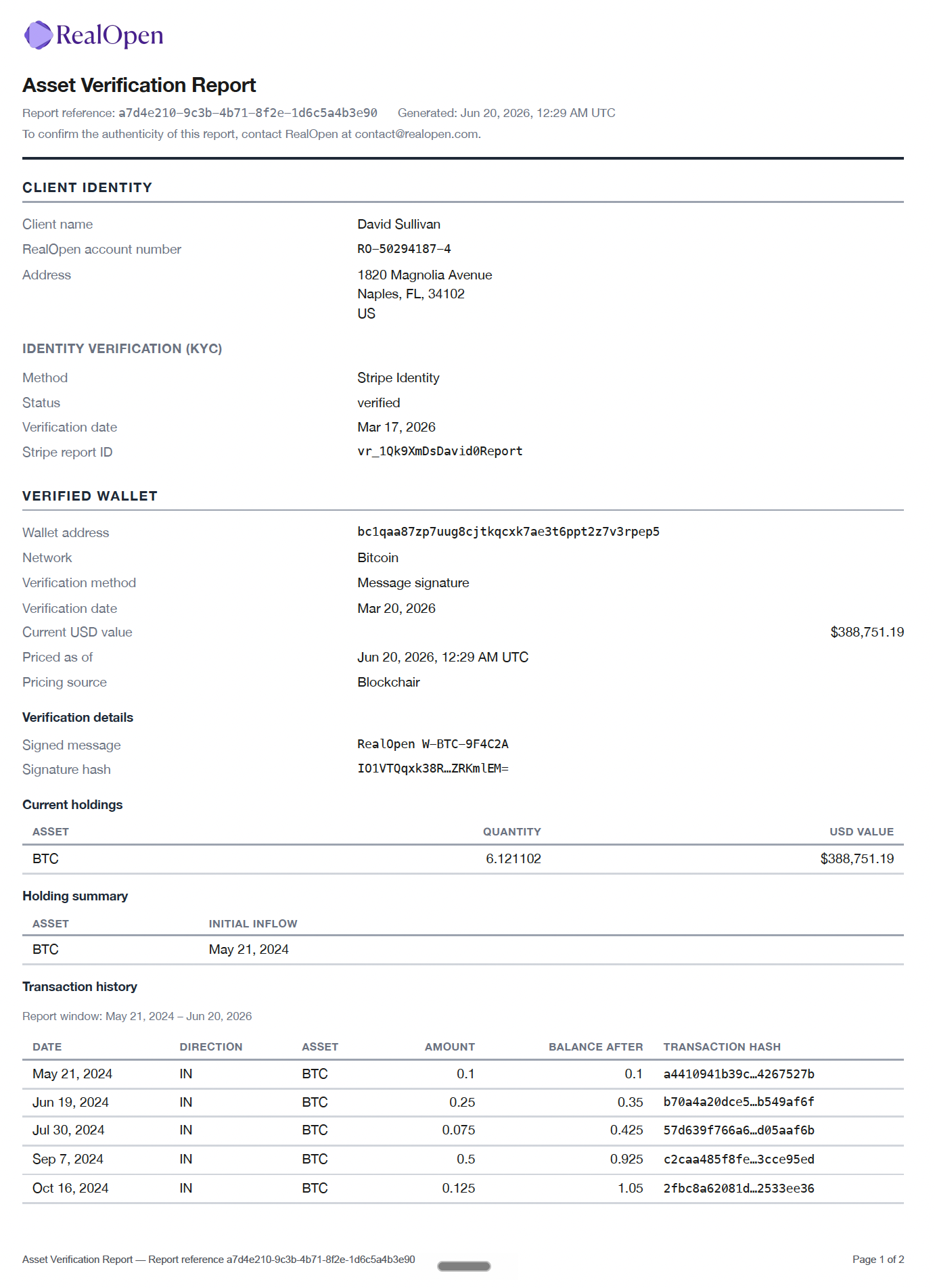

Here's what the Asset Verification Report looks like for a mortgage lender:

Same buyer, same verified holdings, but formatted for the mortgage underwriter. This is what lets them use their crypto to qualify for a loan instead of going full cash.

Here's the trend we're seeing: most crypto buyers aren't going full cash. They're using crypto as down payment and reserves, then financing the rest traditionally.

Your buyer gets verified, converts their crypto to dollars, wires it to escrow for down payment, and then qualifies for a mortgage like anyone else. Underwriter gets an Asset Verification Report showing where the down payment came from. Everyone's happy.

This is actually bigger volume than pure crypto deals. If you've got a buyer with strong income but unusual assets, crypto verification gets them to the finish line faster.

Same way you have a loan officer, a title company, and a home inspector, you've got a crypto guy. That's us.

When a buyer asks if you take crypto, the answer is: "Let me connect you with my team. They handle this stuff, and they're fast."

Ready to get started?